Private Equity Invests for Speed and Predictability

- Jeff Waggoner

- May 5, 2018

- 10 min read

Many would identify Venture Capital as a subset of Private Equity and act as if they are the same business model with minor variations. There’s much alike in the two business models; but the underlying philosophy, scale, operating model, and the firms and leaders in the two spaces are very different. In this post, I will explore the Private Equity and highlight a few differences between VC and PE. I explain Venture Capital’s approaches in a previous post here.

It’s worth starting with the very different roles these two models of investment play. Venture is focused on taking problems in our economy and turning them into thriving businesses from scratch. Private Equity is focused on using leverage to acquire companies, combining them, and tuning their combined operational model to drive EBITDA and value growth through structured performance improvement. This blog will focus on the way Private Equity focuses on leverage and a structured toolkit of performance improvement methodologies to drive value.

As before, I will start with the caveat that there are a very wide variety of models and I will focus below on only one as a generalized example.

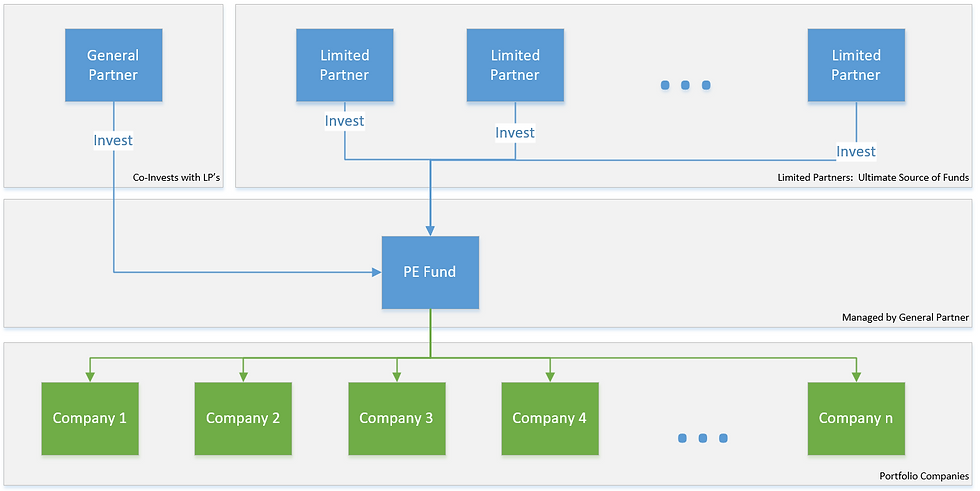

Figure 1 General Investment Entity Structure

Private Equity General Partners invest alongside their Limited Partners. While this can be and often is the case in Venture, the alignment of interests it creates is an important element of risk management for PE Limited Partners. Additionally, while many Venture General Partners will manage multiple funds simultaneously, it is most often in the overlap between fund periods; in PE funds, simultaneous fund development is more the norm. What most people see as the PE fund is the General Partner (GP) and their associated staff. They run the fund, make the investment decisions, and participate in the governance of the portfolio companies. Limited Partners (LP) provide sourcing guarantees for the majority of the funds. Limited Partners can be a great many different types of entities including mutual funds, endowments, pension funds, corporations, banks, or other investment companies. The risk return profile of PE tends to attract more traditional, risk averse investment vehicles. LPs have little knowledge of and no involvement with the portfolio companies. PE Funds are started by raising a fund, the GP defines the funds focus and investment guidelines and forecasts a financial return profile and seeks LP’s to invest in the fund. The funds invested into the fund are subject to a management fee around 2% ±; these fees pay for the staff, offices, and other expenses of running the General Partner Staff’s activity relative to the fund. Some PE firms charge an additional fee to the portfolio company for board and management oversight of the portfolio company as PE firms tend to be more actively involved in the governance and management of their portfolio companies.

Rather than a structured model of investing ever larger amounts as risk is retired, Private Equity seeks to make every investment provide expected fund performance, while still expecting some variation in return. The most common theme is speed and predictability.

The following is an idealized example of a $100M fund; this is a very small fund for Private Equity, but is useful for comparison to the Venture example I’ve given previously. The Limited Partner Agreement allows for 2% annual management fees, a 20% carried interest, and a 6 year hold with a 10% return hurdle rate and 5% General Partner Commitment. The fund’s portfolio strategy is to invest in platforms with annual EBITDA greater than $2M to support a 6.0 Debt/EBITDA ratio for the initial and add-on acquisitions. The fund targets platform hold periods of 4 years and acquires 10 platforms in the first two years.

Figure 2: Idealized Example of $100M small Private Equity Fund Financials

After investments and exit proceeds as well as management fees, the fund has been grown to $171M. On liquidation, the Limited Partners receive 100% of their original capital first ($93M) with the fund’s return hurdle rate of 10% for $102M. The remaining $63M is split between the Limited and General Partners according to the carried interest terms resulting in an additional $50.6M to the Limited Partners and $12.7M to the General Partner. For the Limited Partners, the result is a 6 year investment of $93M that returned 11.7%. This return outperforms the trailing S&P 500 performance by over 7% according to a 2017 study by Bain Insights. For the General Partner, a $5M investment yields a return of $17.7M for an IRR of 28.7% along with $12M in management fees as well as any fees charged to the portfolio companies for governance and management.

The results of the platform companies were dispersed with 20% returning outsized returns (> 60% IRR), 10% (~ 45% IRR), 20% (~ 25% IRR), and the other half of the portfolio providing poor returns with 30% returning their original investment (~0% IRR), and another 20% resulting in loss of investment. While it is true that Private Equity funds focus on risk management, and the risk profile bears a lower risk than Venture, it is hardly risk-free.

Private Equity uses a wide variety of models and approaches. All of them start with an investment thesis that focuses on acquiring one or more companies, with sufficient EBITDA to sustain debt service, and a plan to create value rapidly. Investment theses are in-depth studies of industry, market, and specific acquisition targets with specific planning for product changes and combinations, service differentiation, operational tuning, and financial engineering designed to acquire a platform and steer that platform into a higher EBITDA, higher growth rate, and more robust EBITDA multiple exit within 4 to 5 years. A common framework for these analyses uses Michael Porter’s 5 Forces Model focusing on the key factors driving industry competitiveness and the opportunity to improve a specific platform. The tools for tuning the platform to this higher valuation include organic growth, profitability and competitive advantage improvements to EBITDA, process reengineering to reduce costs, improved responsiveness and flexibility reduce working capital, and add-on Mergers and Acquisitions to enhance value delivery, reduce cost, and/or improve positioning.

The degree of search and planning to identify the correct platform, investment thesis, value creation roadmap, build relationships with that platform, and validate the assumptions and conditions in the investment thesis makes PE investing a slower process in many cases. It is also why many PE firms seek innovative ways to source these opportunities efficiently leveraging industry insiders with the knowledge of the industry, the opportunities, as well as the PE model.

Because of the wide variety of tools employed and approaches taken, there is no well-evolved model of corporate development that can be used as a framework other than to say that speed, predictability, and risk management are key facets of PE portfolio transformation. Typically, a portfolio company lifecycle would require approximately 18 months for platform and pre-planned add-on stabilizations, 18 months to complete all product, service, and process improvements, and 18 months to generate EBITDA growth and prepare the company for exit. PE funds look for platforms with untapped potential from a track record of less disciplined management, strategic errors made earlier in the platform company’s history, continued growth paths, or the ability to unlock new growth from the introduction of the capital that enables a more competitive solution set.

The tools of value creation and business improvement are discussed further below and include:

Leverage

Organic Growth

EBITDA / Gross Margin Improvements

Financial Improvements

Competitive Positioning

The right set of tools to employ and the order in which to employ them can vary tremendously across industry, stage of growth, and platform company history.

Leverage:

The usage of leverage in Private Equity is a key financial tool to enhance the returns. The usage of debt leverage allows acquisitions to be partially financed with debt service covered by the free cash flow of the company; this leverage provides a multiplier on the cash investment in the acquisition. As of the writing of this post, market conditions are allowing Debt to EBITDA ratios of around 5.5 to 6.0; depending on the valuation EBITDA multiple, this can support an acquisition where PE fund cash is used for 35% to 65% of the acquisition costs. The usage of leverage and the additional financial performance covenants adds to the impetus of PE portfolio companies to evolve and perform with great consistency and predictability.

Organic Growth:

The objective behind organic growth is to drive revenue growth with its associated EBITDA growth. Organic growth can be the result of several different strategies. It can come from the introduction of peripheral products and services to existing customers, expansion into new customer segments or entirely new markets, professionalization of the sales and marketing processes, M&A or operational improvements for enhanced product and service competitiveness, and improvements to capital efficiency of scaling to accelerate growth.

Another potential benefit to improvements to the capital efficiency of the company’s scaling can be enhanced EBITDA multiples. Upon exit, the valuation of the company can be influenced by the company’s track record of unit EBITDA (EBITDA associated with the sale of a unit of the company’s product or service) enhancement and capacity to grow efficiently combined with a credible roadmap of future growth and enhancement. These influences can have the effect of raising the effective multiplier on EBITDA; resulting in greater value creation and harvest.

EBITDA / Gross Margin Improvements:

The objective to EBITDA / Gross Margin improvements is to raise the unit Gross Margin / EBITDA of the company’s products and service to drive greater growth, debt service, internal improvements, and ultimately valuation. Such improvements can be found in a great many strategies; depending on the nature of the industry, company approach, and the corporate development history of the company. These strategies can be summarized into the general categories of Cost reduction, Pricing, and Risk Management.

For many companies, a review, redesign, and automation / digital transformation of an appropriate subset of internal processes can yield significant cost savings, faster cycle times, improved customer satisfaction, and increased throughput. As with all process initiatives, it is critical to be aware of which processes are best optimized and which processes require greater flexibility and freedom. Digital transformation is one method of automating the internal and external core processes of the company for marketing, sales, product/service delivery, support, and customer relationship management. For many, even technology focused companies, there are significant swathes of these processes that can be improved through a holistic end-end review and redesign of the entire order to cash process. For production oriented companies, optimizing the throughput and utilization can provide significant positive financial impact. Finally, a regular review of expenses throughout the company can yield significant cost reductions.

Product and Service pricing can yield significant additional value creation for the company. In concert with the approaches for organic growth, performing deep analyses of the market, identifying customer niches and the understanding the value perception map of the product across those niches can enable targeted price adjustments, re-adjustments to the proof of performance for the products / services, additional value creation product roadmaps, and expansion into new adjacent and other markets.

Risk Management can also improve profitability through mitigation and avoidance of downside risks, recognition and value-capture of customer risks being borne by the company, and the associated processes improvements that can be driven by risk management methods.

Financial Improvements:

Financial Improvements increase value by increasing profitability and decreasing the capital required to drive growth and sustain the business; these changes can improve EBITDA, improve the effective EBITDA multiplier from valuation, and improve competitiveness.

The process changes noted above to shrink the order to cash process not only increase the velocity of revenue and customer responsiveness, they usually also decrease working capital per unit of revenue lowering the cost of growth. More overt changes can also improve working capital such as tighter inventory and expenditure control in the customer fulfillment process, redesigning the invoicing milestone and payment process, and assessing any cash holding or escrow provisions in the normal course of fulfillment. For capital intensive businesses, there can be a tremendous opportunity in reducing annual capital expenditure by better utilization and shifting to pay as you consume models where they are financially beneficial.

Competitive Positioning:

Competitive positioning changes unlocks the ability to deliver greater value, charge higher prices, and expand into peripheral products in existing customers and markets as well as peripheral markets. All of these drive EBITDA growth as well as top line Revenue growth, but also risk reduction from market position and/or customer concentration. These changes can be broken down into optimizing product / service development / sales / fulfillment, tighter market segmentation and targeting, improving the organization’s performance organically, or M&A to acquire new skills, products, capabilities, and market share.

Optimizing the product / service development / fulfillment process includes accelerating the concept to market cycle time (product management, development, fulfillment preparation), the flexibility of the product and/or service through the introduction of the ability to customize solutions, reduction of lead times through better inventory management and production cycle time, and targeting the right level of quality for the target market / value proposition. This can also include enhancements to the process of business development within the company; focused on identifying new products in existing markets, new markets to address, and the development of partnerships for solution blending and sales channels for greater market penetration acceleration and competitive strength.

Along with these changes can come organic process improvement, the introduction of new skills and personnel, and the introduction of tools and methodologies to accelerate performance. These changes not only increase enterprise agility, but reduce cost and increase the effectivity of innovation investments.

An additional approach to increased competitive positioning is the usage of strategic acquisitions. This can be to acquire and integrate value-critical functionality to enhance the positioning of the product / service, the rapid introduction of critically needed skills and capabilities, or the acquisition of market share. While M&A can be a very effective means of rapidly gaining these benefits, it can also introduce significant risk, costs, and distraction.

Summary

Private Equity funds seek investments where there are substantial opportunities to rapidly increase value through a lower risk, structured approach to value creation. While there isn’t a single roadmap reference model, there are useful models that various investors try and prove and tend to be copied. While it certainly makes sense to learn from successful models, there also tends to be common themes that are driven by broad market and macro-economic conditions.

PE investments have always used some degree of leverage, but as debt providers have adjusted their maximum Debt to EBITDA ratios down in anticipation of economic challenges in the coming few years, and Venture Companies have become better at professionalization and value harvest along with the record-high valuations from the glut of dry powder cash in the market, the model has shifted more towards growth and less toward cost reduction. Either way, expect Private Equity Investors to be extremely results oriented, impatient, and intolerant to missed projections, but also expect a team culture where a uniting common goal drives a great deal of support from the investment team. This type of approach can prove highly beneficial for a company in the right place with the right mindset and its stakeholders.

In future blogs I will look at the strategic planning and execution using the tools noted in this post, and many other topics relevant to this model. If you would like to discuss how your company is evolving, need help with any of the tools noted above, or just have a question please contact us.

Comments